An unsurprising statement from a financial regulator is sending some welcome signals that point to a spurt of innovation ahead.

The U.S. Office of the Comptroller of the Currency (OCC) issued a statement earlier this week saying that national banks can provide services to stablecoin issuers in the U.S.

This is not a surprise, as banks have been doing so for some time. But they have been doing so under a cloud of regulatory uncertainty. The statement gives the first sign of official clarity on the idea that stablecoins are legitimate representations of value.

Acceptance and support

Why is this significant for markets?

To start with, it signals a growing regulatory acceptance of stablecoins. While fiat-backed blockchain-based tokens have been often talked about in the halls of power, especially after Facebook’s stablecoin project Libra was announced last year, they had not been recognized in an official statement as an acceptable result of financial innovation – until now.

And the U.S. is not the only significant economic bloc to signal acceptance: Earlier this week, the European Central Bank (ECB) issued a report that assesses the threats stablecoins could pose. But rather than hint that stablecoins might be in trouble, the report conveys that the ECB is figuring out how to mitigate the potential risks.

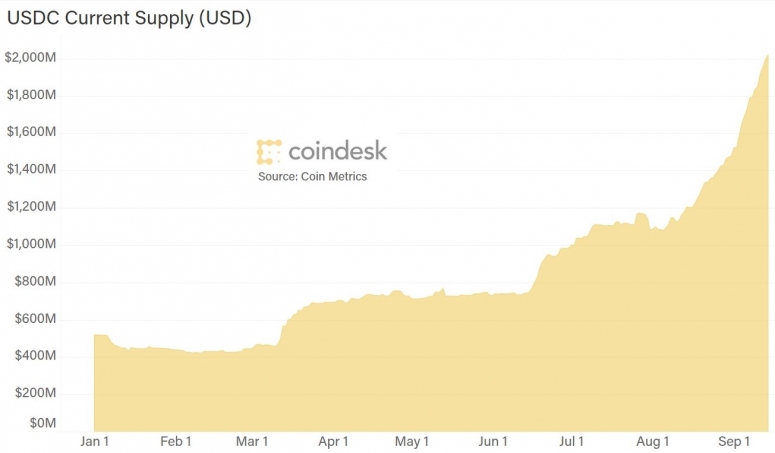

The issue was becoming urgent, given the explosive increase in stablecoin demand. The total value of stablecoins has now surpassed $18 billion, up from $10 billion just four months ago. Much of this growth has been driven by international demand for dollars as well as the increasingly sophisticated financial tools being built on top of public blockchain technology. USDC, the leading U.S.-based stablecoin, has seen its market cap almost quadruple so far this year, to over $2 billion.

Reading between the lines, the message goes even further. Acceptance is one thing; support is another. The OCC is signaling to banks that stablecoin activity is legitimate, and that reserve accounts will be offered the same federal protections as any other.

This could incentivize banks to actively seek stablecoin business, and in so doing, broaden both their client base and their stake in crypto markets.

A recent statement from the OCC said that U.S. national banks could now custody crypto assets. Presumably that includes stablecoins, too. So, a bank could attract not just stablecoin issuers, but also their clients. It would then make sense to facilitate the transfers of stablecoins between clients, and (why not) even between banks. New payments networks could emerge, which in turn could give rise to a host of new banking services. For an industry squeezed by low interest rates and looming defaults, this potential growth vector will eventually start to look attractive.

And since one of the main use cases today for U.S.-based stablecoin USDC (the second largest stablecoin by market cap) is extracting yield from decentralized finance (DeFi) platforms, this could be the incentive needed for traditional finance to start to take an open-minded look at the innovations going on in blockchain-based financial applications. New clients could be courted with new types of savings products, which could in turn accelerate the transformation of traditional banking.

Growth and innovation

It could also embolden new types of stablecoin issuers to come forward with further innovations. To those of us working in the industry, it may seem like stablecoin issuers are everywhere. Looking in from the outside, however, most of them are either small, offshore or both. Other than the members of USDC issuer CENTRE Consortium, founded by Coinbase and Circle in 2018, there are few large U.S.-based corporations commercially active in the space.

Last year, we reported that IBM was building support for a network of stablecoin-issuing banks, and that Wells Fargo had created a corporate stablecoin for internal cross-border transfers.

JPMorgan is apparently still working on JPM Coin, also designed for cross-border payments between institutional clients, announced in 2019. Visa is looking at ways to harness the potential of stablecoins for B2B payments. The list goes on, but no large corporation has yet successfully launched a stablecoin with real-world traction. That is likely to change.

Blockchain-based tokens to represent internal transfers is a relatively straightforward application, and just the tip of what’s possible. An as-yet unexplored option is that of programmable monetary instruments, such as stablecoins that have embedded KYC, or stablecoins that could be distributed amongst certain communities for specific uses limited by code. The OCC statement is likely to give momentum to collaboration between corporations and their banks on creative payments and engagement tools.

The fine line between securities and stablecoins with features is no doubt a factor holding back many private projects. There seems to be regulatory progress there, too. The U.S. Securities and Exchange Commission said this week that they are open to discussions with stablecoin issuers as to whether or not their token would classify as a security – which implies that some would not. While not exactly clarity, it does open the regulatory door to more conversations about innovation at the highest levels, as well as case-by-case decisions that, while slow, would at least give a more solid foundation for development.

Gaps and standards

There are barriers, however.

The infrastructure is still young, and although it is growing rapidly in both scope and scalability, the public blockchains on which most current stablecoins run have scalability issues which at times can push up fees to uncomfortable levels. And, given recent progress in payments infrastructure, stablecoin payments may end up being slower than paying by some more traditional methods.

Stablecoin settlement is also still an issue. The U.S. Uniform Commercial Code (UCC) covers settlement finality (a legal construct that defines the point after which a transaction cannot be reversed) for private systems, but does not address the issue of blockchain settlement finality. With proof-of-work blockchains, settlement is probabilistic, not definite, until a certain number of blocks have passed. And even then, time just makes it increasingly unlikely that a transaction can be reversed. At what stage does a blockchain-based transaction become totally irrevocable? This is understandably an important issue for market participants.

And for many use cases, using stablecoins could add a middleman, rather than streamline operations. This could further impact costs, especially if different fiat currencies are at either end of a transaction.

The potential utility in cross-border transfers highlights the need for an international framework if these instruments are to fulfill their potential to streamline flows of capital. Earlier this month, the Governor of the Bank of England called for a G20 mandate for standard-setting bodies to clarify standards.

In April, the Financial Stability Board (FSB) published the responses to its public consultation on global stablecoin regulation, which make for constructive reading. While not a regulator, the FSB monitors the global financial system and makes recommendations to protect its stability and integrity, and its work could provide a structure for international cooperation.

And regulators will always be concerned about the fragility risks that growing stablecoin popularity could introduce into the global financial system.

A welcome start

Regulatory clarity of any sort is an underappreciated trigger for innovation. True, the crypto industry has no shortage of creative code and ambitious applications. It also has no shortage of people willing to put time and money into devising new applications for new types of value. And the whirlwind of activity going on in the decentralized finance space is generating astonishing growth – since the start of 2020, value locked in DeFi contracts has increased from roughly $675 million to over $8 billion.

But that is still a small speck in the financial universe. Adoption and impactful applications will not make a meaningful impact on finance until regulatory clarity encourages serious money to take notice.

I struggled to come up with a metaphor that could represent this type of trigger, one that did not involve everything falling down (which means dominoes are out), things blowing up (the spark in the fireworks shed won’t do) or anything to do with viral contagion (because obviously).

In the end, the best I could come up with was a seed that becomes a tree that is so impressive it encourages planters in other regions to plant their own. This image is lacking in oomph and sparkle, but finance moves slowly. And even a forest of new trees would not convey the scale of innovation that we could be on the verge of seeing. It is hopefully a reminder, though, that meaningful and long-lasting change starts small.

A comprehensive crypto industry overview

The University of Cambridge’s latest industry survey is out, with no shortage of surprising findings. This is their third edition, and compiles data from 280 entities from 59 countries, across four market segments: exchange, payments, custody and mining. It’s an insightful overview into how crypto businesses are faring around the world, and highlights some interesting trends.

- Full-time employee growth slowed to 21% in 2019, down from 57% in 2018. The decline was especially notable in smaller firms, which implies that a few large players are dominating the industry.

- On average, 39% of proof-of-work mining is powered by renewable energy, primarily hydroelectric, while 76% of miners say they use some form of renewables in their energy mix. This is up from 28% and 60%, respectively, in 2018.

- Approximately 13% of miners now use financial products such as hashrate or crypto asset derivatives to hedge risks.

- Capital expenditures take up to 56% of U.S.-based miner costs, compared to 31% for Chinese miners, which suggests a competitive edge for Chinese miners that could be explained by the concentration of hardware manufacturers in China.

- 55% of surveyed service providers now support stablecoins, up from 11% in 2018.

- An estimate of the number of crypto asset users has been updated to 101 million identified users, up from 35 million in 2018. This is due to an increase in the number of active accounts, and to more rigorous compliance with KYC procedures on the part of service providers.

- Service providers operationally headquartered in North America and Europe indicate that business and institutional clients make up 30% of their customers. This figure is much lower for Asia-Pacific and Latin American firms, at 16% and 10% respectively.

- Compliance with KYC/AML obligations is heterogeneous across regions. Nearly all customer accounts at European and North American service providers have been KYC’ed, whereas this is the case for only one out of two accounts at service providers based in the Middle East and Africa. The share of crypto asset-only companies that did not conduct any KYC checks at all dropped from 48% to 13% between 2018 and 2020.

- 46% of service providers report not being insured against any risks. 90% keep crypto asset funds in cold storage. 45% use a third-party crypto custodian as part of their cold storage system.

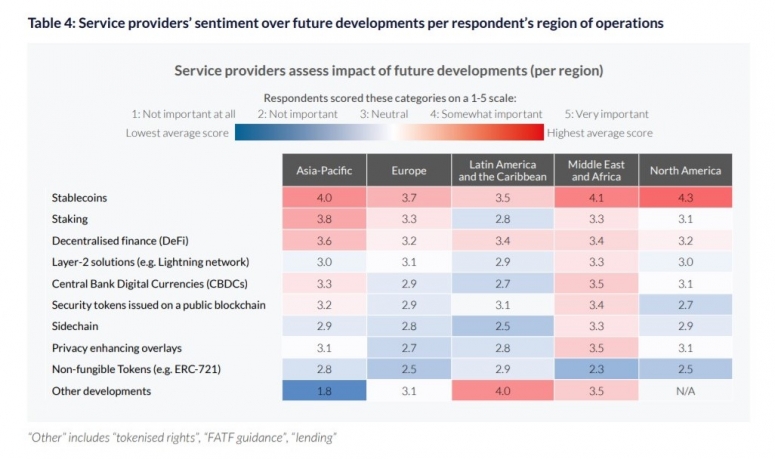

One of my favorite parts of the report was this chart, which color-codes the importance crypto service providers assign to various trends emerging in the industry. Stablecoins win, not surprisingly. Staking and security tokens got less interest than I expected. And the relative lack of interest in non-fungible tokens hints that the recent market buzz around the concept may be short-lived.

A recommendable and eye-opening read.

Anyone know what’s going on yet?

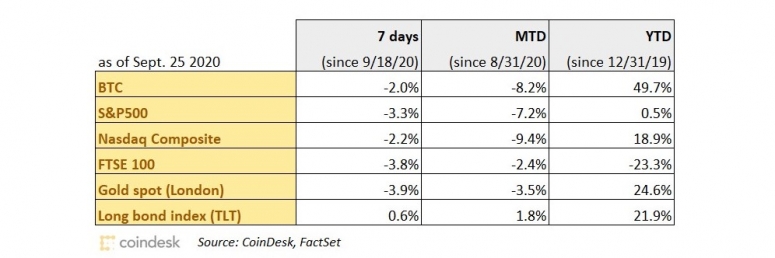

This week’s sell off in equity markets felt different from previous half-hearted declines. The scope, combined with the intensifying concern in various media around the likelihood of a contested U.S. election, a disappointing vaccine and repeated lockdowns, feels more like a change of sentiment that could, in the absence of generous stimulus checks, snowball into genuine worry about the state of the global economy.

Related to this, I’ve spent some time recently wondering what will drive the stock markets after the pandemic is over. Rebuilding? Infrastrtucture hasn’t been damaged. Consumption? Many spending habits will have permanently changed. And what of all the companies that can’t support employee costs once federal aid is not on the table?

Of course there will be success stories, and of course emerging technologies will continue to present growth plays. But are the future earnings that current valuations are pointing to realistic?

Bitcoin fared better than most other assets this past week, but that’s not saying much.

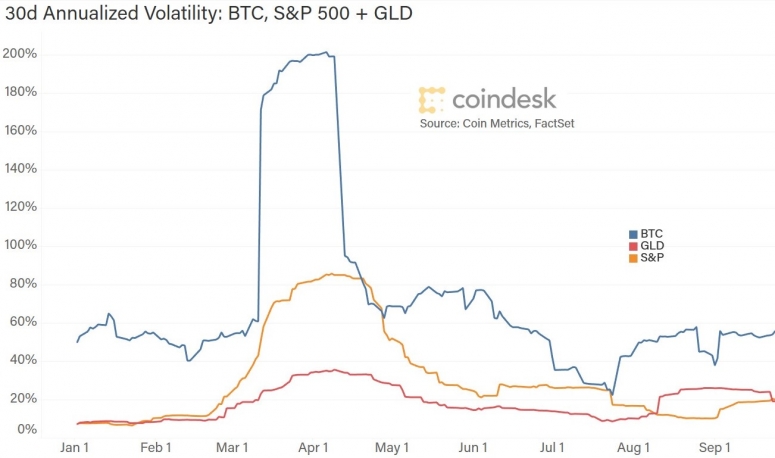

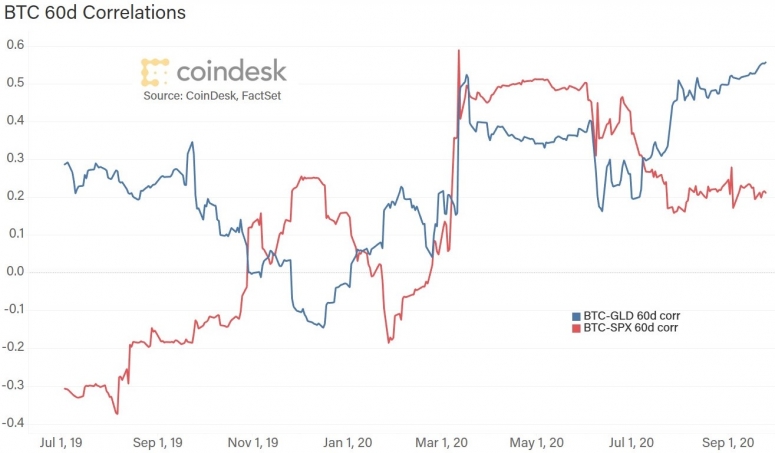

This feels like a good time to revisit bitcoin’s volatility compared to gold and the S&P 500.

Given the swings in the BTC price over the past week, it’s not surprising that volatility is edging up. Gold’s volatility, on the other hand, is edging down.

To further confuse the narrative, the 60d correlation between the natural log returns of BTC and gold continues to increase, while the correlation with the S&P 500 is holding steady. For now.

(Note: Nothing in this newsletter is investment advice. The author owns some bitcoin and ether.)

CHAIN LINKS

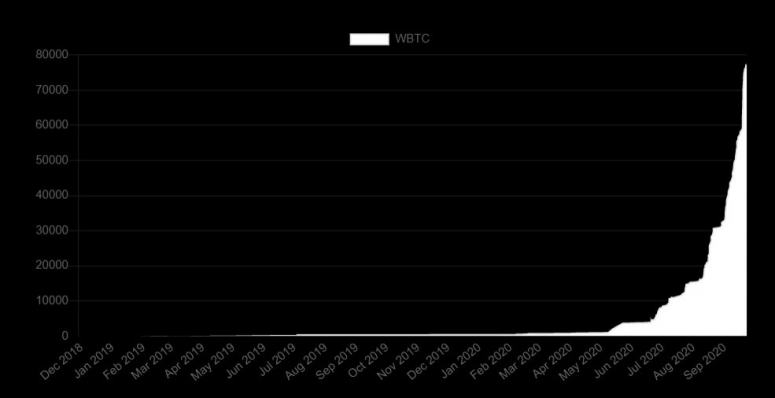

The flow of bitcoin onto Ethereum continues to astonish – this week the market value of bitcoin that has been adapted to work on the Ethereum blockchain passed $1 billion. TAKEAWAY: I’ve written about the phenomenon of Ethereum-based bitcoin before, and am not surprised to see this level of growth. Why would anyone want to put their BTC on Ethereum, you ask? Because Ethereum-based tokens can participate in the myriad decentralized finance (DeFi) lending protocols that pay yields on deposits. Yes, BTC can earn a yield. There are risks – DeFi is still a young, niche application with counterparty and technology risk, as well as regulatory uncertainty. But for many, the yield and the innovation are compelling.

The most liquid bitcoin-on-Ethereum token is wrapped bitcoin (wBTC), managed by crypto custodian BitGo. There are other options, however, such as tBTC, which this week relaunched with a system that relies on a decentralized network of nodes, wallets and smart contracts.

This week alone, over $170 million was added to wBTC, according to btconethereum.com. Investment fund Three Arrows Capital accounted for almost $25 million-worth of that, setting an individual wBTC transaction record just one week after Alameda Research minted almost $22 million worth. (Update: Alameda then upped Three Arrows Capital’s transaction, and I’ve given up trying to keep up.)

Now, the concept is spreading to other blockchains: BitGo will enable wBTC on the Tron blockchain, with the aim of boosting its decentralized finance ecosystem. Tron currently has much lower fees than Ethereum – but the persistent popularity of stablecoins on Ethereum vs. Tron shows that the market on the whole doesn’t seem to mind.

The Digital Commodity Exchange Act of 2020, introduced this week by Rep. Michael Conaway (R-Texas), seeks to create a federal definition of “digital commodity exchanges,” putting them in their own legal category and charging the Commodity Futures Trading Commission (CFTC) with oversight. TAKEAWAY: If passed, this would finally establish a regulator for cryptocurrencies. So far, they’ve been languishing in no-man’s land, which has hindered market infrastructure development. Many U.S.-based institutions cannot transact on an unregulated exchange, which puts crypto exchanges out of bounds: They may be licensed, but without a regulator, they are unregulated. Federal regulation would also ease many of the burdens U.S.-based crypto exchanges face, such as the need to go state by state for permission to transact.

The European Commission has proposed a bill that would provide clarity on crypto asset definitions, rules on digital asset custody as well as details on what the relationship between token issuers and holders should be. If passed, this would turn the EU into the largest and most significant regulated space for cryptocurrencies anywhere in the world. TAKEAWAY: The regulatory clarity is coming thick and fast these days. This is good news for an asset group that promises global access. Institutional support for that global access will boost funding, infrastructure investment and, eventually, adoption.

Social Capital, a California-based investment firm that purchased bitcoin in 2013, is considering going public.TAKEAWAY: The firm, which specializes in technology startups, earlier this month filed three new Special Purpose Acquisition Companies (SPACs) with the SEC, bringing his firm’s total up to six. It also announced that one of the SPACs was merging with Opendoor (his first merged with Virgin Atlantic earlier this year) and hinted in an interview that he is thinking of taking the whole firm public. If this comes to pass, it would be the first publicly traded venture capital and private equity fund manager with a significant market value to invest in cryptocurrency. It is unclear how much bitcoin Social Capital owns, but an investor letter in 2018 said that one of Social Capital’s largest investments was in bitcoin, so – considering when it was first bought – it’s probably quite a lot.

Some veteran FX traders are moving into the cryptocurrency space because of its volatility. TAKEAWAY: A reminder that volatility is not necessarily bad. We tend to equate volatility with risk (I’ve written about this before), which has negative connotations – you don’t often hear about investment advisors talking about risk to the upside. But high volatility means swings up as well as swings down, and seasoned traders pride themselves on their ability to harness the upside while protecting the downside. The growth of hedging instruments and the smoother flows on market infrastructure make the volatility more manageable than back in the early days. Inexperienced traders can truly suffer, though, as volatility can turn against you at a moment’s notice.

The cryptocurrency money manager Panxora seeks to raise up to $50 million for a new hedge fund to buy digital tokens associated with the fast-growing decentralized finance (DeFi) sector. TAKEAWAY: So far, decentralized finance (DeFi) tokens have been the purview of crypto enthusiasts and some professional investors chasing higher yields. This type of fund is one of the first but is unlikely to be the last that hopes to bring institutional money into the space. Whether the market’s liquidity can handle that kind of volume remains to be seen. According to crypto data provider Messari, the total reported market cap of DeFi tokens is over $5 billion, with over $600 million in 24-hr trading volume, so it can probably handle an inflow of $50 million without too much chaos. This is worth watching, though, as the next funds of this ilk might be more ambitious.

The Bermuda Stock Exchange (BSX) has accepted its first crypto asset exchange-traded fund (ETF), Hashdex Nasdaq Crypto Index ETF. TAKEAWAY: The BMX is not a large stock exchange – its aggregate market cap is just under $300 million. A total of 3 million shares is available via private placement at $1,000 each. So, doing the math, this ETF – if completely sold – would multiply the market cap of the entire stock exchange by more than 10x. I don’t want to be a downer, but isn’t that a bit ambitious?

Podcast episodes worth listening to:

And CoinDesk as not one but three new podcast series that are definitely worth checking out and subscribing to:

- Money Reimagined, with Michael Casey and Sheila Warren of the WEF – for the first episode, they talk to multimedia artist Nicky Enright and University of Virginia Media Studies Professor Lana Swartz

- Borderless, with Nik De, Anna Baydakova and Danny Nelson, which covers trends impacting crypto adoption around the world

- Opinionated, with Ben Schiller – for the first episode, he interviews Nic Carter, CoinDesk columnist and partner of Castle Island Ventures